Virtually all our nation’s leaders talk about valuing children and families. America ought to be a place where the birth of a child is a glorious event, rather than the beginning of a family’s economic ruin. “25% of poverty spells begin with the birth of a child” – National Partnership for Women and Families. While I can’t reverse years of institutional knowledge control, I can share what I know in the hopes that it helps you and your family.

This is a guest post from my husband, Jason. Jason’s favorite hobbies are Peloton (check out the Best Peloton Instructors Based on Your Mood) and talking finance. While he works in corporate strategic financial planning, he is not a personal financial consultant and these opinions are his own.

This is not an article about teaching your children about money, it’s a resource for new parents to help budget for your new baby.

Why you should read this

I’m Jason, husband of New Modern Mom, Barbara, and I’ve spent the better part of my life employed in some way or another focused on Finance. I was fortunate to grow up in a household where there was an endless amount of financial discussions, full of plenty of business jargon. This led to my passion for business and solving problems.

I’ve worked at all kinds of companies, big and small. I grasp every opportunity to discuss finances and love to learn more about them partially because I’m a total finance geek and also because I see how much can be gained by understanding the system.

How does all that qualify me to talk about budgeting for your baby? It doesn’t, but hopefully you find some of my experience and advice useful.

The scariest thing about having a baby is…

One of the scariest things about having a baby is the financial pressures related to bringing a new life into this world. The first thing you need to know is that everyone’s finances are 100% personal to them. No two families have the exact same financial situation. Why don’t they teach personal finance in school? My friends and I theorize that it’s a conspiracy to build a greater wealth divide, and that’s possible, but if anything it's a huge oversight.

Some considerations for new parents to budgeting for your new baby: estimating the medical costs associated with having children (and after), planning for parental leave, and budgeting for all of your new baby’s life expenses. Just check Barbara’s baby registry checklist, it adds up fast. Looking beyond just your baby’s first year, there are constant expenses related to diapers, clothes, toys, activities, schooling and even food (children eat A LOT).

Some things are easy to learn, such as how to change the stinkiest of diapers and get consistent burps, but other things take a lot of meticulous planning and rightfully so since they can have a BIG impact down the line.

There are so many blogs, podcasts, websites, and books dedicated to personal finances, I recommend you educate yourself as much as possible. You and your children’s future depends on what you do now. The earlier you think about budgeting for your family, the larger the impact will be. Take a deep breath and let's dive in.

14 considerations when budgeting for your baby as new parents

1. Understand your health insurance and anticipate the costs.

This includes optimizing what healthcare plan you’re on – which usually means adjusting to have the lowest “max out of pocket” + “monthly premium” available to you at your next life event or annual plan selection. In the U.S., the average new mother with insurance will pay more than $4,500 for her labor and delivery, a new study in Health Affairs has found. This can vary greatly depending on your insurance, so definitely get into the details of your own plan and familiarize yourself with insurance invoices. Lastly, don’t be afraid to call the provider (hospital) and insurance company to ask questions and challenge the bill. Roughly 80 percent of all medical bills contain billing errors – healthcareinamerica.us. Click here to learn more about average costs of giving birth.

2. Plan for maternity and paternity leave.

How much time you and your partner get off work for parental leave, whether you’re paid during that period, how much you’re paid, and whether you are a primary caregiver can all significantly impact your household finances in the coming year. Understand your company’s policies and your state’s laws to get an accurate picture of how your maternity or paternity leave will affect your bottom line. You apply through your State and each is unique with potentially more than one program covering you such as both “disability” and “paid family leave”. State’s often have tight windows to apply such as 30 days, so be sure you research ahead of time. Also look into whether your particular benefit is taxable. Most EDD (Employment Development Department) (or similar in your state) benefits are taxable, but not all.

3. Draft your baby budget.

One time costs such as hospital visits, pre-baby doctor appointments, cribs, changing table, nursing chair… recurring costs such as childcare, diapers, wipes, formula, baby doctor visits, constantly larger clothes… Wow, this list is overwhelming! These are all just a scratch on the surface of the ever growing costs. Use your favorite spreadsheet app (excel, numbers, google sheets) to budget out every cost you can think of that is new to your family. Make sure to track against your overall budget, ask family and friends for help, borrow items when possible and my personal favorite is to buy used. Babies go through things so fast as they grow that used items are often just as good at half the price. We’ve found that Facebook Marketplace is much better than Craigslist or Letgo. We’ve also found that childcare is the most expensive recurring cost.

Take an honest look at your expected costs and what your financial state will be with your baby. Be realistic with yourselves, you and your partner will certainly need to make some cuts.

Everyone’s budget is different depending on where you live, what help you get, used/new, and quality, however I’ve put together this example budget to get you started HERE.

4. Choose a Pediatrician in your insurance network.

Your baby’s first doctor appointment will come within their first week of life, so you’ll want to have a pediatrician picked out. I know it sounds odd, but the hospital will sometimes not release you until you have a follow up appointment either with them or your pediatrician scheduled for 48-72 hours after discharge. Using Teledoc, OneMedical, or other services like this will often significantly lower your costs in the long run, even with upfront fees. For instance, everytime we go to a pediatrician appointment in person and haven't hit our “Max Out of Pocket,” it might cost us a few hundred dollars. If we use OneMedical video visit through their app we almost always can find a solution to our medical concerns and pay nothing, zero dollars. This is great for eye infections, running noses, and small rashes. Not sponsored, but feel free to use my OneMedical referral code by clicking here to get $25 off your annual membership.

5. Start your emergency fund.

If you don’t already have a “rainy day fund,” now’s the time to anticipate some emergencies. Children are accident prone, and with the cost of raising a child there’s no telling if you’ll have the disposable income to pay for any unexpected expenses. Having at least three to six months’ worth of living expenses covered is a great place to start. If you are having trouble saving, try a few of these recommendations from Mint:

6. Order a birth certificate and Social Security card immediately.

The main focus while you’re in the hospital is having a healthy baby. But there are a few loose ends that will need to be taken care of. Hospital staffers should provide you with the necessary paperwork to get your new child’s Social Security number and birth certificate. Usually if you ask them to process the paperwork, they will do most of the leg work for you. If they don’t or if you are having a home birth, contact your state or county office of vital records for the birth certificate and your local Social Security office to get a Social Security card. In our case, about 8-12 weeks after our baby’s birth we had to submit a physical form to the Social Security Office to get his Social Security Card and then had to submit another physical form with a cashiers check (yes, who uses cashier checks still?) to our local county office. Cashier checks can be purchased at the Post Office. Wikihow has a good article on the topic here.

7. Add your child to your health insurance.

In most cases, you have 30 days from your child’s birth to add him to an existing health insurance policy. In some employer-based plans, you have 60 days. Regardless, do it sooner rather than later, as you don’t want to be caught with a sick baby and no coverage. Don’t worry if you do this after birth, your costs from his first appointment should still be covered under the parents until they have their own.

8. Consider a life insurance policy on your child.

There are a lot of costs to incur prior to considering life insurance, but if you manage to still have funds left over, this could be a savior you didn’t realize you needed until you need it most. Considering tragedy at such a joyous time seems really out of place which is why many parents don’t plan for it. When it comes to covering children, a “term” policy that lasts until they are self-sufficient is the most popular choice, but if you can afford it, “whole” life insurance is a better plan and a way to invest in their future.

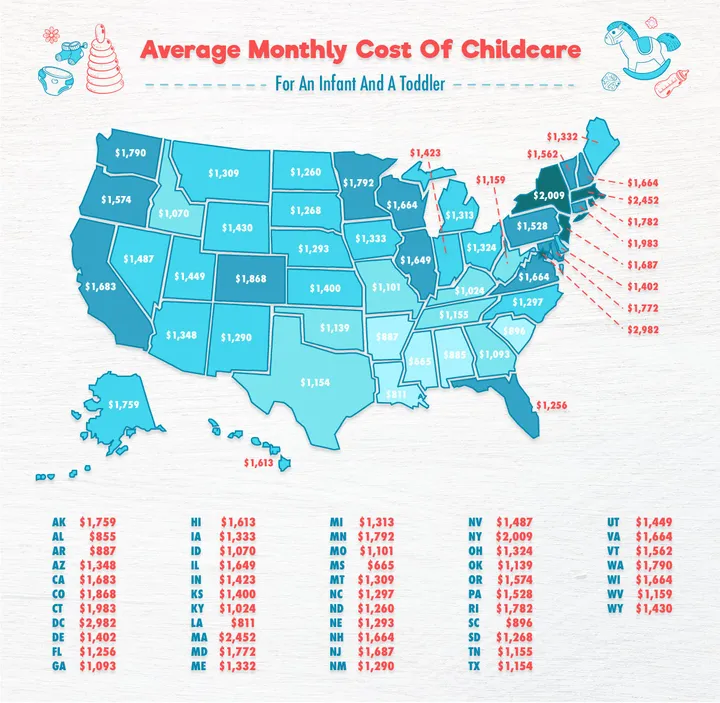

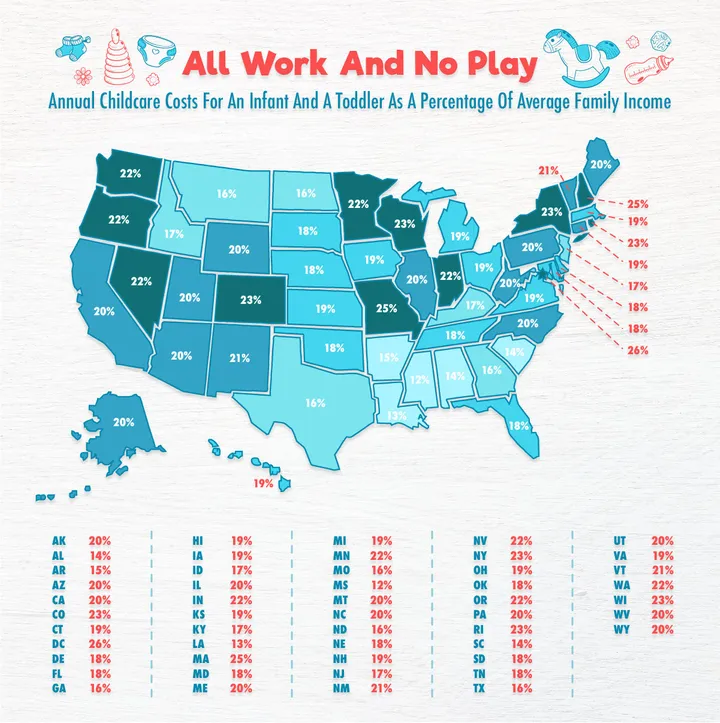

9. Begin planning for childcare.

Make sure to take advantage of the Childcare FSA that allows you to put away pre-tax dollars to pay for childcare ($5k for joint parents and $2.5k if just one). You don’t want just anybody to watch your little rascal and the right person or place can add up. Finding the right daycare or nanny can take weeks. The average annual cost of center-based infant care in the U.S. is $11,959, according to Child Care Aware. But if you live in any large city, you know childcare is easily triple if not quadruple that cost!

Get started long before your maternity leave is over. You’ll need time to visit day cares, interview nannies/Au Pairs, as well as complete an application and approval process if required. Barbara will be writing about our process finding a nanny and Au Pair at a later time, so let's talk about Finances.

Great article and images by Huffington Post here.

10. Adjust your beneficiaries.

Assuming you already have life insurance for yourself or the main breadwinner in your household — and if you don’t, you should — you may want to add your child as a beneficiary. The same goes for your 401(k) and IRAs. However, keep in mind that you’ll need to make adjustments elsewhere to ensure when and how your child will have access to the money. A will and/or trust can accomplish this (point 11).

11. Write or adjust your will.

Tragic things happen and you want to ensure your child is taken care of in the event that one or both parents die. Designate a guardian so the courts don’t have to. Your will is only one part of estate planning, but it’s a good place to begin. In addition to a Living Will, many people create a trust to avoid a thing called probate. If you don’t own a home and only have bank accounts or brokerage accounts, adding your family as beneficiaries there has a similar impact. If you do own your own home you should consider doing the “holy trinity” – Will/Living Will, Healthcare Directive, Family Trust. If you’re in California happy to share who we used, DM Barbara @newmodernmom on Instagram for a referral.

12. Keep funding your retirement and consider funding your kids’.

When your little bundle of joy arrives, it’s easy to forget your personal goals and long-term plans in light of this huge responsibility. If you don't have any, it’s time to make some. You now have more than just yourselves to think about. Stay on top of your retirement plans so your child doesn’t have to support you in old age. If eligible, consider your contributions to a 401(k), 401(b), Roth-401(k), IRA, SEP IRA, Simple IRA.

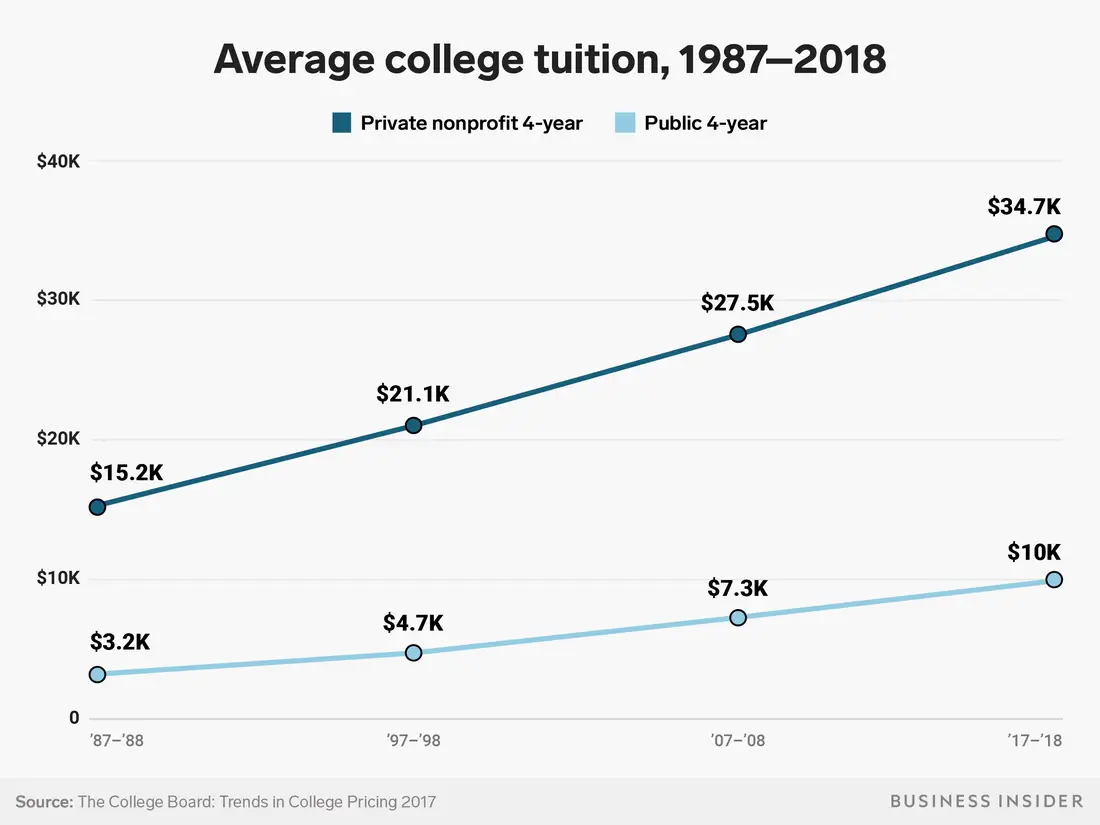

13. Save for his or her education.

College is costly, but you can make it more manageable by starting to save early.

529 Account: These are accounts that grow tax free and are usually either run by financial institutions (think Fidelity or Charles Schwab) or individual State’s. I recommend sticking to the State options because they tend to have lower management fees. We chose to use the California one. Even though this account has tax-free growth and is sponsored by California, we can actually use the funds to send our little one to college anywhere.

The big argument I always hear is “what if my kid doesn’t go to college or gets a scholarship?” Answer: 1. If the account beneficiary does not attend college, the account owner may change the beneficiary to another eligible family member (I know I linked to it, but it’s pretty much anyone in your family, including your kids’ kids). 2. You can take the money out and you just pay the taxes you would have paid anyways. Per Scholarshare site: “Taxable withdrawals are withdrawals due to the beneficiary's death, permanent disability, receipt of a scholarship award, or attendance at a military academy. A taxable withdrawal will be subject to applicable federal income tax on earnings, if any, but will not be subject to the 10% additional federal tax on earnings (the “Additional Tax”).”

HERE is a worksheet that allows you figure out how much to put away upfront or monthly in order to pay for your child’s education when they’re 18. Thank you to my friend Mike for sharing this spreadsheet.

Instructions for use:

- Make a copy of google sheet.

- In cell B2 enter what you expect the total cost of college to be in 18 years.

- Adjust cell B1 if you want to get specific about what interest you think the account will earn. 4% to be conservative, 6% to be aggressive.

- Use the far left two columns to see what you would need to put in the plan if contributing all up front, second two if it’s just monthly, and third two (far right) if you do a combo of upfront contribution and monthly.

14. Make sure you get the Childcare Tax Credit on your Annual Taxes.

The IRS urges people not to overlook the Child and Dependent Care Tax Credit. Eligible taxpayers may be able claim it if they paid for someone to care for a child, dependent or spouse last year. IRS website here:

Taxpayers can use the IRS Interactive Tax Assistant tool, Am I Eligible to Claim the Child and Dependent Care Credit?, to help determine if they are eligible to claim the credit for expenses paid for the care of an individual to allow the taxpayer to work or look for work.

Now that we’ve done all of that it’s time to sit back and have a cold apple juice. Cheers.

Jason

New Modern Dad